We bring character, we exhibit camaraderie, we serve to protect the community

||| FROM AMY TAYLOR for SAN JUAN ISLAND FIRE & RESCUE |||

Executive Summary

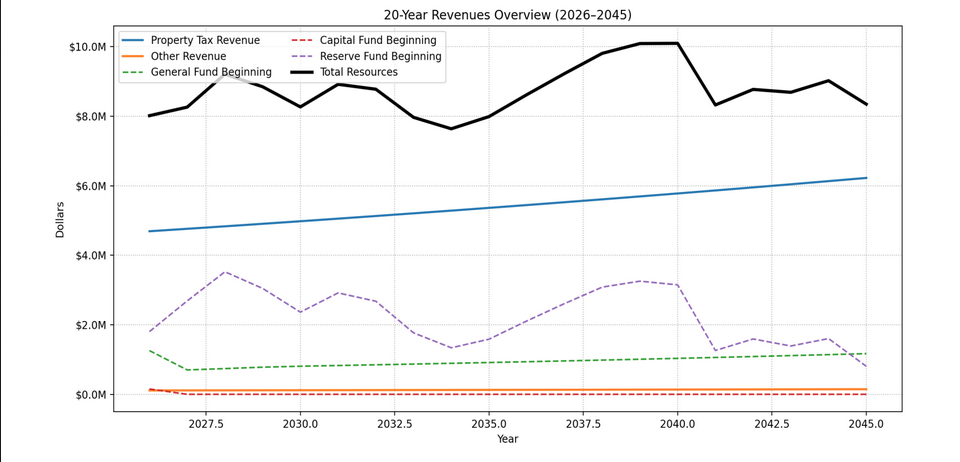

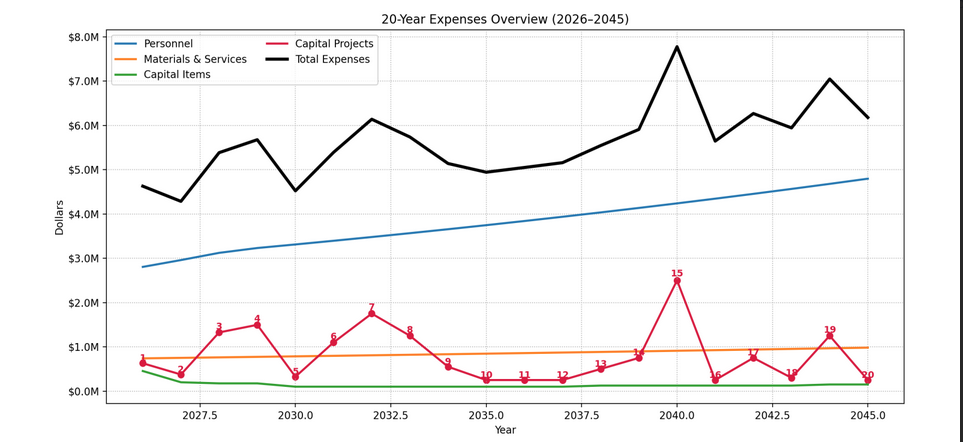

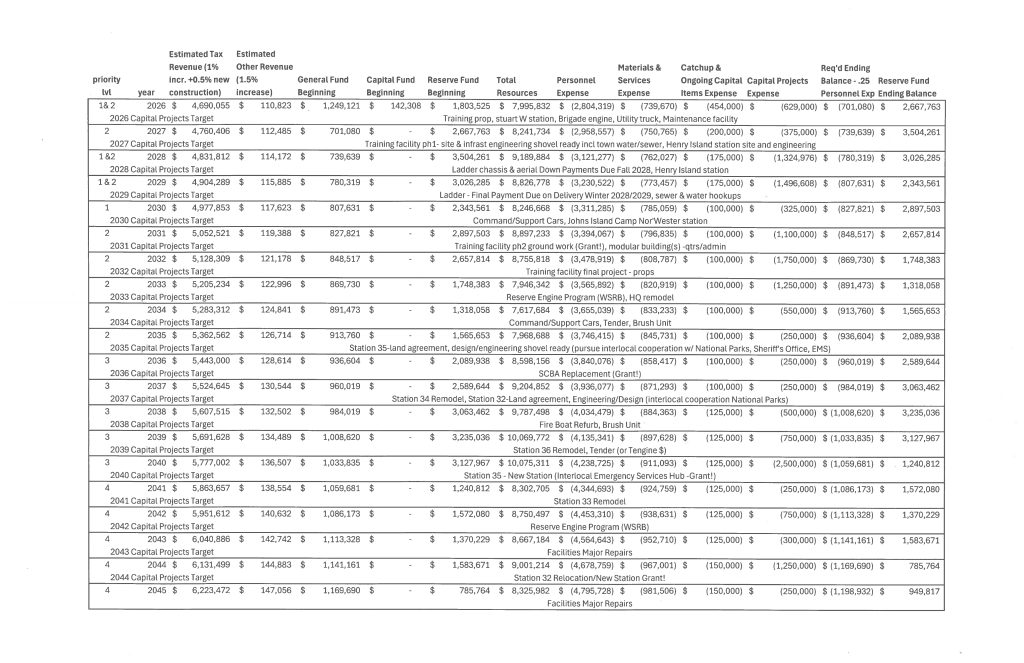

This plan summarizes projected revenues and expenditures over twenty years. All figures are based on the 2026 Budget.

The plan provides an annual estimate which considers the listed Key Baseline Assumptions. The intent is to provide the Board of Commissioners with projected financial stability in their ongoing oversight of ensuring stable all-hazard emergency services to the public within the jurisdiction. The plan is a living document, which will require periodic review and adjustment depending on economic fluctuations that affect revenue and expenses. The plan should minimally be reviewed every five years and continued an additional five years.

Tax revenues are assumed to remain stable at up to 1% increase each year, however determined by the Board. Risk of lost tax revenue due to decrease in property values is unlikely because the levy is currently less than half the maximum allowed. Target annual new building construction tax revenue at 0.5% is conservative, based on long-term averages.

Key Baseline Assumptions:

- Property tax revenue grows at ~1.0% plus 0.5% new construction annually.

- Reserve fund investments grow at 2.5%

- Other revenues including leasehold tax, reimbursements, and compensable services grow at ~1.5% annually.

- Grants, donations, gifts, are not included. Several Capital Projects are Grant aligned.

- Beginning fund balances maintain 25% annual personnel expense.

- Annual personnel expenses increase by 5.5% initially to meet new staff merit increases, then reduce to 2.5% sustained.

- Materials and services expenses increase by 1.5% annually.

- Capital items expenses are front loaded with various catchup projects then reduced to meet need.

- Capital project expenses are detailed in the Expenditure Outlook below and assume all things being equal.

- Reserve funds are maintained in investments to cover planned capital expenses or unforeseen events.

- Additional ending balance resources may be allocated to Reserve Funds, improve services, or pay off principle.

Revenue Outlook

Key Considerations

- Plan assumes all things being equal. Revenues match long-term averages, however new construction and interest income fluctuations are anticipated.

- The ongoing volunteer staffing model is stressed and may require reductions to outer station and fleet capital expense outlay if minimum staffing levels are not met.

- Volunteers provide significant work output in the logistical and administrative functions of the agency, which otherwise may require additional paid staff or reduction in services.

- Personnel costs may need periodic adjustments to maintain competitive hiring and retention.

- Plan assumes use of internal resources only. Loans may be explored to stretch capital projects expenses and align financial stability.

- Shovel ready projects and projects that collaborate with other agencies are objective grant targets.

- Utilizing fleet reserve plan and fleet refurbishment while meeting target WSRB criteria results in considerable capital expense reduction.

- Active participation in Washington State Mobilization will result substantively in reduced personnel expenses and increased revenues.

- Expanding tax exempt entities impact resources operationally and financially. The Fire District protects the County’s only incorporated Town, the County Seat, other comparatively large public districts, and various County, State, and Federal lands – all of which do not contribute to property tax assessments.

Attachment:

**If you are reading theOrcasonian for free, thank your fellow islanders. If you would like to support theOrcasonian CLICK HERE to set your modestly-priced, voluntary subscription. Otherwise, no worries; we’re happy to share with you.**